Leverage Existing Client Data to Grow Your Business

In today’s competitive financial services environment, data is a powerful tool to attract and retain clients. Financial professionals who understand… Read More

Insights and best practices for successful financial planning engagement

• Joe Buhrmann • December 12, 2023

What separates the elite practice from the ordinary? That would be a financial advisor business plan, according to consulting firm CEG Worldwide. They found that 70 percent of the top-earning advisors have both formal business plans and formal marketing plans. Though a written advisor business plan alone is not enough to equal success, this evidence suggests that planning provides important clarity and discipline.

A financial planner business plan forces you to evaluate many areas of your business at once, from your mission and value proposition to your operations and marketing. This broad overview helps you take an intentional approach to growing a sustainable business.

Maybe you’re thinking that your business plan is simple enough to keep in your head, and writing down a formal plan isn’t necessary. If that’s the case, I have a quote for you from Dwight D. Eisenhower: “In preparing for battle I have always found that plans are useless, but planning is indispensable.”

Consider these five main subjects as the template for a streamlined financial advisor business plan. Although there are many more you could potentially include, these are the most impactful.

Knowing the characteristics of your ideal client, you can build a practice to suit their exact needs. That’s why step one in the process is getting a handle on who it is you serve best.

Research from Kitces.com shows advisors with a niche achieve greater efficiency and can charge more for their advice.2 Their analysts found that a top niche advisor makes $660,000 on average, versus a generalist advisor at an average income of $142,500.

A recent Cerulli survey of RIAs showed many are trying to break into a niche market but find it challenging to adapt their core business components, including service offerings, marketing, and business development. The research found that 49 percent of RIAs don’t work with niche client segments.3 The remaining advisors were able to select all niche groups they specialize in:

That “other” niche might be as specific as “travel-loving young families” (Experience Your Wealth), or it could be as general as “people over age 50 who value financial advice.” Reflect on which clients you most enjoy working with and build a specialty planning practice that can address and even anticipate their needs.

Defining who you will serve will provide the foundation for your unique value proposition—the answer to the question “Why should I work with you?”

The secret to standing out in the marketplace is to emphasize the expertise you have or the type of client you work with. Here are a few examples:

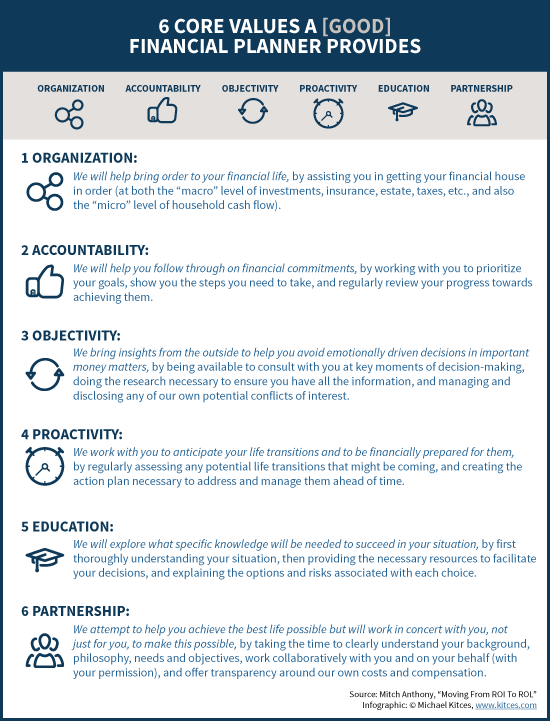

Prospects who see themselves reflected in these profiles will find these value propositions compelling. It’s clear that you’re a great fit for them, aiding in any comparison with a generalist advisor. (For more on this topic, see Kitces.com’s 6 Core Values a Good Financial Planner Provides.)

Now it’s time to design a tech stack that supports your value proposition. You’ll need the big three: a CRM, a financial planning platform (ideally one with a client portal and aggregation), and a portfolio management tool. Here’s where you ask yourself: Do I want my tech to battle the financial complexities of life like soldiers in bright red uniforms that march in straight lines, or do I want tech wearing camouflage with the capability and flexibility to work in many situations, from mass affluent investors on up to ultra-high net worth? When building your financial planner tech stack, think about:

Efficiency. What tools integrate well to save time and hassle? That goes for you as the advisor, as well as for clients. Our latest research shows advisors (and clients alike) see efficiency gains from having a client portal, for example.4

Flexibility. It’s important to take into account alternative ways of charging for planning to keep up with industry norms and have a planning platform that can provide value no matter the fee structure.

Comprehensiveness. It’s better to have the feature and not need it than to need it and not have it. You can buy software that will handle 90 percent of what you need to do, but it’s that 10 percent you can’t do that will come back to haunt you, especially as your clients’ needs and wealth grow over time. Getting a second platform is not efficient or cost-effective. No single platform makes it easy to switch to another. When it comes to financial planning platforms in particular, which provide a good deal of differentiation for an advisor, being able to meet the evolving needs of your clients is crucial. If you ever foresee a time when you’ll be creating extensive, holistic financial plans, choose your tech accordingly.

What you’ve created so far (a target market or niche, a UVP, and an ideal tech stack) will now feed into your marketing plan, the strategy that’s going to help you reach prospects who will hopefully become clients. This is how you’ll communicate your brand and value to the world and measure the results to determine your return on investment.

First, think about what you want to achieve. Are you looking to grow? What kind of pace of growth can you and your firm handle? How many clients can you add before you hit a tipping point?

Then, think about different ways you might achieve your goals. How will you reach your ideal audience of prospects? What platforms do they spend their time on? What are their interests? Let the answers guide what marketing tactics you try first. (To see what strategies other advisors have found recent success with, including LinkedIn campaigns and livestreams, read Six Advisor Marketing Ideas Revealed on Reddit.)

Finally, you should define upfront what success looks like for your marketing efforts. Consider measuring what you can control. For example, if you’re trying to attract clients through social media content, you can set a goal of creating two to four pieces of content a week or dedicate a set amount of time each week to engage with prospects there. Another idea is to measure booked meetings with prospects.

After giving your strategy time to work, you can measure the resources spent versus the prospects gained to determine ROI.

Now it’s time to define how you’ll measure the overall success of your business plan. If your overall goal is to achieve $1 billion in assets under management and create a firm that will carry on your legacy, that’s one thing. It’s an entirely different goal to build a solopreneur practice that sustains your family’s standard of living and serves people you enjoy working with.

To get a handle on how you might benchmark your practice, read Financial Planning KPIs Your Firm Should Be Tracking. It explores metrics you might not have thought of such as next-generation client relationship rate.

If your ultimate goal is to create an exceptional client experience, read about how service KPIs, such as Net Promoter Score and referrals per client, can be telling.

You know it’s not wise to give clients 27 financial planning recommendations at once. No human being can keep their eye on 27 different things. In the same way, you have to intentionally focus your attention and energy on only a handful of the most urgent and important items for your business, the things that will move the needle.

You’ve probably heard of the metaphor of rocks, pebbles, and sand in a jar, used to illustrate prioritization: The jar represents your life, and the contents represent the things that fill it. If not, here’s Stephen Covey’s version of that exercise in a video format. The message is to focus on the big things in life first to make sure you can fit them in.

Once you’ve identified the metaphorical “big rocks” to focus on (from business development to financial planning), think about how you can streamline using technology and repeatable processes for the rest, or maybe even outsource tasks if necessary.

Having a service calendar, and making sure everyone in your practice knows their role in delivering those services, can help create a consistent client experience. From paraplanner to service assistant, each member of your team should know their role and be empowered to execute it to a level of excellence.

As a financial planner, a bit of “back of the napkin” math should be second nature. Working up a quick budget (what are you spending per month on E&O insurance, technology, designations), as well as financial projections for the business, can ground you in knowing where you are. Repeated each year, you can start to see where you’re headed.

As your practice matures, you can add other forward-thinking aspects to this plan, such as business continuity planning and succession planning. But for now, focus on the big rocks as outlined above. When you define these important aspects in a written advisor business plan, you’ll have clarity for the road ahead.

To continue your improvement journey, check out our eBook “Using the Data You Have to Evolve Your Business and Client Relationships.” This guide shows you how you can use key data points, technology, and repeatable workflows to make financial planning a reality for every client.

Sources:

1. CEG Worldwide / Meridian-IQ. “Best Practices of Elite Financial Advisors,” 2012.

2. Kitces.com. “Kitces Research On Advantages Of Niching In Time Use, Planning Approach, Pricing, and Productivity,” August 2020.

3. The Cerulli Report. “U.S. RIA Marketplace 2023,” November 2023.

4. eMoney Beyond the Plan Research Study, June 2023, n=1,507.

DISCLAIMER: The eMoney Advisor Blog is meant as an educational and informative resource for financial professionals and individuals alike. It is not meant to be, and should not be taken as financial, legal, tax or other professional advice. Those seeking professional advice may do so by consulting with a professional advisor. eMoney Advisor will not be liable for any actions you may take based on the content of this blog.

You may also be interested in...

In today’s competitive financial services environment, data is a powerful tool to attract and retain clients. Financial professionals who understand… Read More

As tax laws evolve, it’s more important than ever for financial professionals to stay current on the latest regulations and… Read More

Most advisors don’t have a growth problem. They have a complexity problem. Financial professionals don’t stall because they lack intelligence… Read More

Download this eBook now and learn how AI is expected to impact the industry.

Download Nowa new source of expert insights for financial professionals.

Get StartedTips specific to the eMoney platform can be found in

the eMoney application, under Help, eMoney Advisor Blog.

{kind=link}